Connecting The Dots Part 6

In this series, we will examine and connect the dots, on several topics, all of which are contributing to stagflation, low interest rates, negative economic growth, and the greatest asset bubbles of all time.

After reviewing The Supply Side Melt Down behind Door #1, and The Reserve Side Melt Up behind Door #2, let's see whats behind the last door #3....

If It's Tuesday, This Must Be Belgium

From Wolf Richter, Foreigners Dump Record Amount Of U.S. Securities, But Who The Heck Is Still Buying?

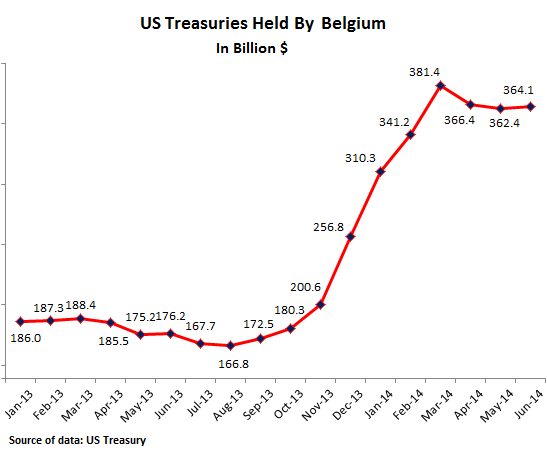

Belgium, thats who. Since October 2013, they have doubled their holdings from $180 to $365 billion to become the 3rd largest foreign holder behind China and Japan.

Is it really Belgium or are they just fronting for China? Who cares, if China wants to bitch about QE and decrease public bond purchases, they are more than making up for it through covert Belgian purchases.

According to the US Treasury, about 53 percent of U.S. long-term debt securities held by foreigners will mature in 5 years or less from June 30, 2009. Foreigners held 18% of outstanding long term debt for a total of $9.5 Trillion x 53% = $5 Trillion.

According to the US Treasury, similar to the June 2012 survey, about 57 percent of U.S. long-term debt securities held by foreigners will mature in 5 years or less from June 30, 2013. Foreigners held 20% of outstanding long term debt for a total of $13.5 Trillion x 57% = $7.7 Trillion.

Note above, over the five year period, nice to pay off all that debt with low value dollars and reissue lower interest debt, isn't it? And now, for a change, a comforting graph, even.

MZM - MSI cost preferred in billions since 1975.

Notice how the MZM monthly services index cost spikes just before or during recessions. It's not spiking now and has never been lower than today. You can take some comfort, that is, if you trust the numbers.

We are in a period of history influenced by demographic shifts, high debt burdens, stagnant productivity and income inequality, during which the central banks introduced liquidity into the system which has suppressed asset volatility, interest rates and encouraged gamblers to leverage.

There is simply too much debt in the system. So much that the Fed is trapped and cannot raise rates by any significant amount. How much could they raise? Judging from their economic projections...

The median estimate by Fed officials was for the fed funds rate to move to 1 percent in December 2015 and 2.25 percent a year later. So, the Fed itself envisions rates near 2% in 2016, and that might be premature.

Back to the debt, with our National Debt at $17.6 trillion and counting, the United States cannot afford higher interest rates. The net interest payments on the debt ($234 billion) would skyrocket.

If rates reverted to the Fed long run average, our interest payments would double, and that’s only if we don’t accumulate any more debt. How much GLOBAL debt is there?

Between mid-2007 and mid-2013 the amount of global debt has soared more than 40 percent to $100 trillion for a $30 trillion increase from $70 trillion.

Did real GDP increase during this period? It declined. Did corporations borrow all that money to facilitate future economic growth? While substituting financial engineering for actual capital spending, (using liabilities to increase share price, rather than meeting needs on the asset side) they lined their wealthy shareholders and executives pockets.

US Total Personal Debt stands at $16.5 trillion, the Total US Debt at $61.6 trillion, with $2.5 trillion in interest cost paid on it thus far.

Higher rates = increasing debt service = borrowing more to pay the interest = higher debt. As the debt continues to accumulate our ability to accommodate interest rate increases, declines by the minute.

With the patient already prone on the table and barely clinging to life by a thread.... rising interest rates would crater the housing market, cause an exodus from equities, precipitating a stock market crash, and the overall economy would cascade into a complete economic collapse.

But it gets better, and it always does... remember from Part 3: as interest rates go up, the velocity of the money in the system goes up?

If the reserves and stock pile of savings aren't drained off, which is impossible because... from 1913 to 2007 the Fed created $800 billion in new money. From 2008 on, the Fed has created on average, $800 billion in new money, EVERY YEAR. That's 94 years worth of money being created every 12 months for the last six years.

Even if the Fed could sop up the excess, rates would go up, the bond market would crash, and the government would not be able to sell enough new bonds to sop up the base of money they have already created.

The bottom line is that the our country cannot afford any significant rate increases. So, hopefully the "experts" at the Fed can continue to thwart market forces and keep control of interest rates. In this scenario, low rates and ZIRP are here to stay.

In any event, the minute rates rise, for any reason, the velocity of just the $10 trillion in US savings alone would cause hyperinflation. But doesn't this benefit borrowers at the expense of lenders, by repaying debt with money of lesser value? In a stagnant economy, this would be another recipe for disaster.

Yes, its 1969 and Suzanne is muy caliente. No that isn't Bob Newhart, its a very young Al Swearengen Aka Ian McShane.

After reviewing The Supply Side Melt Down behind Door #1, and The Reserve Side Melt Up behind Door #2, let's see whats behind the last door #3....

If It's Tuesday, This Must Be Belgium

From Wolf Richter, Foreigners Dump Record Amount Of U.S. Securities, But Who The Heck Is Still Buying?

Belgium, thats who. Since October 2013, they have doubled their holdings from $180 to $365 billion to become the 3rd largest foreign holder behind China and Japan.

Is it really Belgium or are they just fronting for China? Who cares, if China wants to bitch about QE and decrease public bond purchases, they are more than making up for it through covert Belgian purchases.

According to the US Treasury, about 53 percent of U.S. long-term debt securities held by foreigners will mature in 5 years or less from June 30, 2009. Foreigners held 18% of outstanding long term debt for a total of $9.5 Trillion x 53% = $5 Trillion.

According to the US Treasury, similar to the June 2012 survey, about 57 percent of U.S. long-term debt securities held by foreigners will mature in 5 years or less from June 30, 2013. Foreigners held 20% of outstanding long term debt for a total of $13.5 Trillion x 57% = $7.7 Trillion.

Note above, over the five year period, nice to pay off all that debt with low value dollars and reissue lower interest debt, isn't it? And now, for a change, a comforting graph, even.

MZM - MSI cost preferred in billions since 1975.

Notice how the MZM monthly services index cost spikes just before or during recessions. It's not spiking now and has never been lower than today. You can take some comfort, that is, if you trust the numbers.

We are in a period of history influenced by demographic shifts, high debt burdens, stagnant productivity and income inequality, during which the central banks introduced liquidity into the system which has suppressed asset volatility, interest rates and encouraged gamblers to leverage.

There is simply too much debt in the system. So much that the Fed is trapped and cannot raise rates by any significant amount. How much could they raise? Judging from their economic projections...

The median estimate by Fed officials was for the fed funds rate to move to 1 percent in December 2015 and 2.25 percent a year later. So, the Fed itself envisions rates near 2% in 2016, and that might be premature.

Back to the debt, with our National Debt at $17.6 trillion and counting, the United States cannot afford higher interest rates. The net interest payments on the debt ($234 billion) would skyrocket.

If rates reverted to the Fed long run average, our interest payments would double, and that’s only if we don’t accumulate any more debt. How much GLOBAL debt is there?

Between mid-2007 and mid-2013 the amount of global debt has soared more than 40 percent to $100 trillion for a $30 trillion increase from $70 trillion.

Did real GDP increase during this period? It declined. Did corporations borrow all that money to facilitate future economic growth? While substituting financial engineering for actual capital spending, (using liabilities to increase share price, rather than meeting needs on the asset side) they lined their wealthy shareholders and executives pockets.

US Total Personal Debt stands at $16.5 trillion, the Total US Debt at $61.6 trillion, with $2.5 trillion in interest cost paid on it thus far.

Higher rates = increasing debt service = borrowing more to pay the interest = higher debt. As the debt continues to accumulate our ability to accommodate interest rate increases, declines by the minute.

With the patient already prone on the table and barely clinging to life by a thread.... rising interest rates would crater the housing market, cause an exodus from equities, precipitating a stock market crash, and the overall economy would cascade into a complete economic collapse.

But it gets better, and it always does... remember from Part 3: as interest rates go up, the velocity of the money in the system goes up?

If the reserves and stock pile of savings aren't drained off, which is impossible because... from 1913 to 2007 the Fed created $800 billion in new money. From 2008 on, the Fed has created on average, $800 billion in new money, EVERY YEAR. That's 94 years worth of money being created every 12 months for the last six years.

Even if the Fed could sop up the excess, rates would go up, the bond market would crash, and the government would not be able to sell enough new bonds to sop up the base of money they have already created.

The bottom line is that the our country cannot afford any significant rate increases. So, hopefully the "experts" at the Fed can continue to thwart market forces and keep control of interest rates. In this scenario, low rates and ZIRP are here to stay.

In any event, the minute rates rise, for any reason, the velocity of just the $10 trillion in US savings alone would cause hyperinflation. But doesn't this benefit borrowers at the expense of lenders, by repaying debt with money of lesser value? In a stagnant economy, this would be another recipe for disaster.

Yes, its 1969 and Suzanne is muy caliente. No that isn't Bob Newhart, its a very young Al Swearengen Aka Ian McShane.

Comments