Commodities Double Whammy

On Seeking Alpha, John Saucer at Mobius Risk Group notes:

Weak economic growth in Europe, China, Japan and other key BRICs .

At present, BOJ is purchasing ¥6 to ¥8 trillion (US $55-$75 billion) of government bonds per month and, with some of its September purchases, the BOJ drove 3-month interest rates into negative territory.

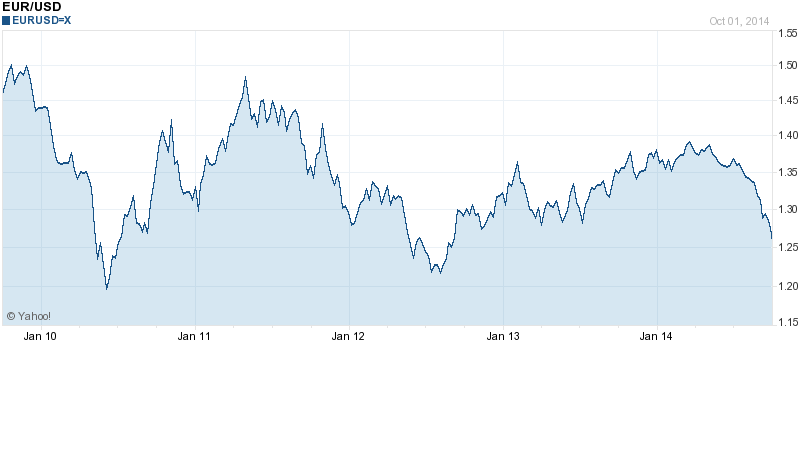

The ECB trimmed its interest rates again earlier this month to -0.2% which pushed the Euro below $1.30 for the first time in more than a year and sent some European bond yields into negative territory. Five year Euro vs Dollar chart below.

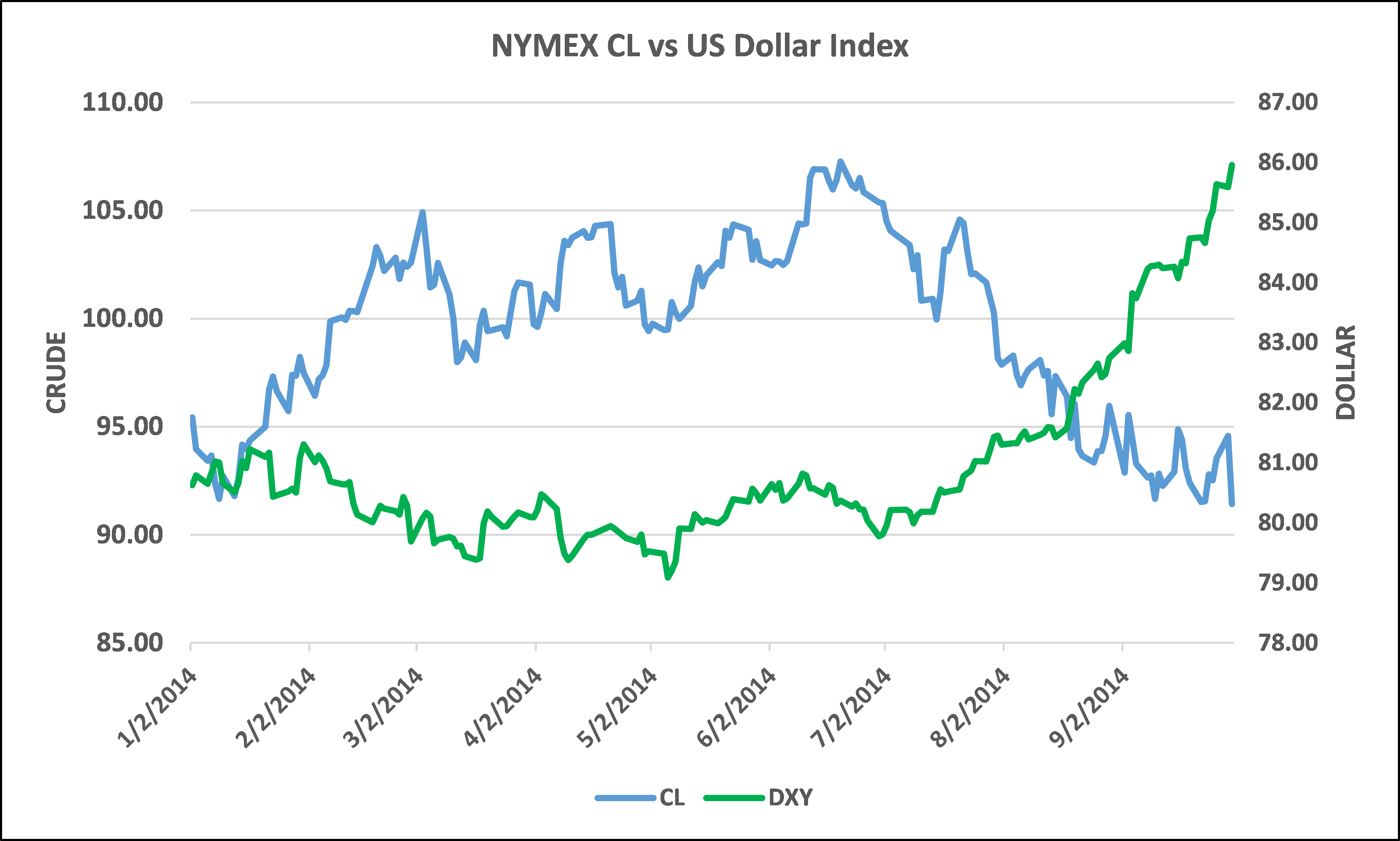

The US Dollar Index (DXY) has since rallied nearly 9% in just over four months. The DXY made new highs for the year this week at 86.22, and the move marks the longest rally phase for the DXY since the index was created in 1973. Nymex crude vs Dollar chart below.

The Nattering One muses... There's a silver lining in every cloud. Generally, equities and commodities have a divergence, they go the opposite way of each other. We are in the midst of a convergence, as both are headed down.

Usually declining commodities means contracting economies. Currently we have a double whammy, add on a strengthening dollar, this means further declining prices in dollar denominated commodities.

This is a good thing as we should see lower prices for goods requiring these inputs. The Saudis may be overpumping to screw the Russians. Still, crude below $75 a barrel for a prolonged period could help resuscitate the economy.

Weak economic growth in Europe, China, Japan and other key BRICs .

At present, BOJ is purchasing ¥6 to ¥8 trillion (US $55-$75 billion) of government bonds per month and, with some of its September purchases, the BOJ drove 3-month interest rates into negative territory.

The ECB trimmed its interest rates again earlier this month to -0.2% which pushed the Euro below $1.30 for the first time in more than a year and sent some European bond yields into negative territory. Five year Euro vs Dollar chart below.

The US Dollar Index (DXY) has since rallied nearly 9% in just over four months. The DXY made new highs for the year this week at 86.22, and the move marks the longest rally phase for the DXY since the index was created in 1973. Nymex crude vs Dollar chart below.

The Nattering One muses... There's a silver lining in every cloud. Generally, equities and commodities have a divergence, they go the opposite way of each other. We are in the midst of a convergence, as both are headed down.

Usually declining commodities means contracting economies. Currently we have a double whammy, add on a strengthening dollar, this means further declining prices in dollar denominated commodities.

This is a good thing as we should see lower prices for goods requiring these inputs. The Saudis may be overpumping to screw the Russians. Still, crude below $75 a barrel for a prolonged period could help resuscitate the economy.

Comments