There Is Something In This More Than Natural - Part 4

Summary

- Of Economic Base Metamorphosis, Capital Misallocation and The McJob Malaise.

- There are unnatural side effects from the interrelationship of QE, ZIRP and Secular Stagnation.

- 35 years of economic deconstruction; the fallacies of central bank policies; and the resulting misallocation of capital; cannot be turned around without a return to the basics.

- An effort must be made to incentivize productive investment and reconstitute a durable domestic economic base.

In Part 1 we examined how it took 25 years of financial deregulation, globalization and outsourcing to labor at the margin to emasculate our durable domestic economic base.

In Part 2 we examined how this morphing effected household income; and how spending patterns were maintained during the period.

In Part 3 we examined the two requirements for a return to economic normalcy.

In Part 4 we answer the multi Trillion dollar question, just where would all this money for these projects come from?

Excerpt from an excellent article in the Financial Times:

Infrastructure came to seem less important during the internet boom of the late 1990s when the economy grew rapidly despite low public investment.

Josh Bivens, at the Economic Policy Institute: “I think the consequence of low public investment is lower productivity growth going forward unless it is reversed."

Chart below: Public investment in the US has hit its lowest level since demobilisation after WW2.

More details on this tragedy of the commons at The Century Foundation and FT.com.

Rather than being invested in R and D, durable economic activity or public infrastructure, FOR WHOM and WHERE did all the money go??

Rather than being invested in R and D, durable economic activity or public infrastructure, FOR WHOM and WHERE did all the money go??

Much of that liquidity, however, has sat fallow. Banks have put away close to $2.8 trillion in reserves, and households are sitting on $2.15 trillion in savings-about a 50 percent increase over the past five years."

Lawrence J. Kramer aptly commented here: We need to make saving less important to savers, as it has already become counterproductive at the aggregate level. Note that all of the arguments about the private savings level are addressed not to lack of resulting capital - we're awash in that...The obvious solution, then, is not to increase saving, but to decrease the personal need for it. Government insurance against the risks we save for would free up tons of money to chase goods and get us going again."

There exists a hoard of Trillions in "easy money" minted and printed which has been misallocated as reserves/passive investment in corporate, financial institution and Fed coffers.

From Wayne Strout, The Mystery of Sustained Low Interest Rates. Insuring the safety of bank deposits by requiring banks to buy government debt tends to produce low interest rates but it does not encourage any expansion in business activity. Increased savings by the public increases bank deposits and ramps up the requirement for banks to hold even more government debt.

To reverse this trend, given the current regulations, the public will need to borrow more and save less.

Unless we see a substantial increase in "animal spirits" leading to both increased borrowing (hopefully for productive activity) and/or decreased savings, it is very possible that we will have low interest rates for a long time. (Animal spirits is an economic term referring to people's willingness to take risks because of an expected future economic boom.) Of course, in such a low interest rate scenario, without such "animal spirits" we will have many banks where most of the depositor's money is simply lent to the government. This is a recipe for economic stagnation.

Rising interest rates will only occur because of increased supply of interest payments (more borrowing) from borrowers and/or decreased demand for them (less lending/saving). (This is a bit counter-intuitive as popular opinion seems to assume that interest rates are low because banks are not lending. Interest rates are low because demand for interest payments from the largest borrowers, namely governments, is increasing.)

The misallocation and perversion of capital refers to the stock of easy money sitting in zero risk and return savings which equates to foregone consumption or productive economic investment. To these ends, as the Bard penned, there is something in this more than natural.

What's wrong is that economists: don’t know the difference between the supply of money & the supply of loan funds; don’t recognize that interest rates are the price of loan-funds, not the price of money; don't realize that inflation is the most important factor determining interest rates, operating as it does through both the demand for and the supply of loan-funds.

Monetary policy became contradictory and perverse, encouraging financial investment (activating portfolio rebalancing), and not income generating investment, or real-investment (new plant and equipment, etc.). I.e., Fed policy elicited income redistribution in reverse ("wealth effect" - sic)."

Due to central bank policies, a prolonged period of ZIRP (zero interest rates) and QE (quantitative easing), this misallocated stock is high, which has spurred misappropriation into undertakings which might never have occurred under normal circumstances, or had normal market forces been at work. We are witnessing the "twinkie market" that Seth Klarman spoke of in 2010 (artificially preserved by unnatural government ingredients).

From IIargi, The Imminent Demise of the American Economy. Companies need to invest their earnings into projects that will generate profits... they can't keep on buying their own shares over and over again.

Much of what they buy back shares with is borrowed money... these allegedly rich firms are loading up on debt. While their productive qualities, for lack of a better term, get thrown out with the bathwater.

...their shares are supposed to represent a certain value, ONLY because they've used their capital, and then leveraged some, to lift those same shares. ...50% of US public pension funds are now holding the same US stocks. Everyone puts lipstick on the US corporate pig.

They're poised to spend $914 billion on share buybacks and dividends this year, or about 95% of earnings... Money returned to stock owners exceeded profits in the first quarter and may again in the third. "You can only go so far with financial engineering before you actually have to have a business with real growth," Chris Bouffard at Mutual Fund Store.

Excluding the recession years 2001 and 2008, dividends and stock buybacks have represented, on average, 85% of corporate earnings since 1998.

Through buybacks, S&P companies have, aided by central banks, and Wall Street, created a hugely perverted idea of what their shares are worth. 'Someone's buying, so there must be value there'. Well, not if the seller poses as the buyer too.

The lack of capital invested in productive undertakings spells even more erosion of the US manufacturing base.

All the easy money has put share buybacks off the charts while CAPEX and R&D have suffered. The distortion of central bank policies has led to malinvestment on the part of corporate management. The consequences of which will be felt when earnings outlooks are reduced because these companies decided to fore go productive capital investment in favor of financial engineering.

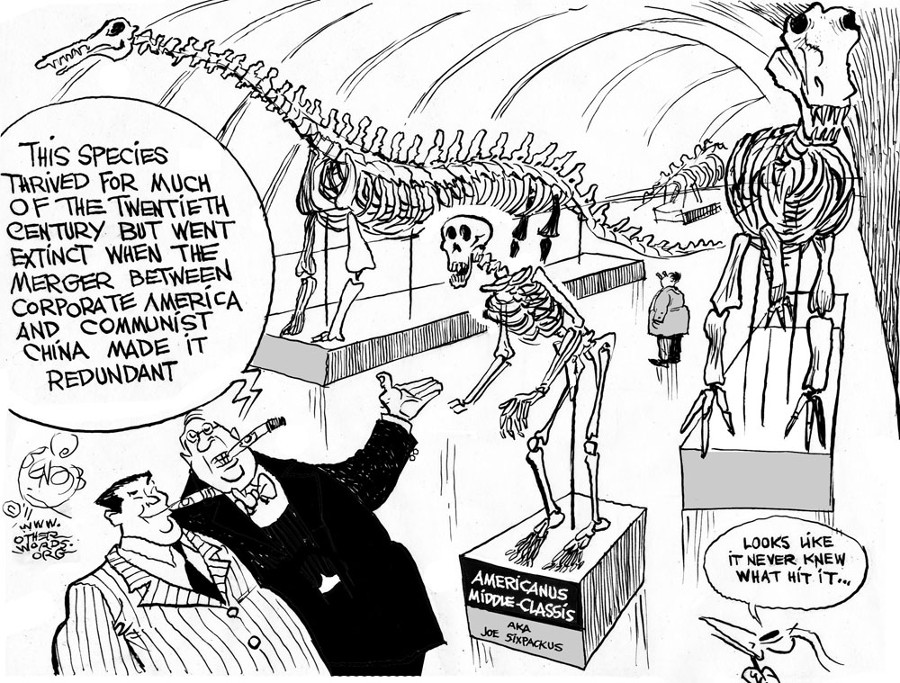

Service sector jobs get a boost while real wealth generating jobs get outsourced. Household income suffers, the middle class gets eradicated along with our future.

Service sector jobs get a boost while real wealth generating jobs get outsourced. Household income suffers, the middle class gets eradicated along with our future.

{kind=link}

{kind=link}

As a society, we need to incentivize productive capital investment in a durable domestic economic base and de-incentivize the need for passive investment. i.e. The money has to be in play and working, if it is, you get rewarded, if its not, you get taxed.

Repeat and rinse, The existing economic McJob malaise is a testimony that:

1. an outsourced service based (hospitality, healthcare) economy wrought with McJobs is not sustainable.

2. primary domicile housing should not be treated as a fungible commodity for speculators.

3. 35 years of economic deconstruction; the fallacies of central bank policies; and the resulting misallocation of capital; cannot be turned around without a return to the basics.

At the end of the day, the stark reality is, there will be no meaningful economic recovery from this McJob malaise of misallocation until at least two conditions are met:

1. housing price/income ratios revert to pre 1995 levels or harmonize.

2. incentivize productive capital investment and reconstitute a durable domestic economic base.

Our economic foundation must be rebuilt upon a stable durable base, anything else would be a highly illusory house of cards and doomed to failure. Repeat and rinse, those who cannot learn from history are doomed to repeat it.

An epilogue to come on the morrow, stay tuned, no flippin

An epilogue to come on the morrow, stay tuned, no flippin

Recommended reading:

Comments