When Frisco Pops, They All Float Down Here

From Dave Kranzler at Seeking Alpha, Housing Update Market: It's Getting Worse :

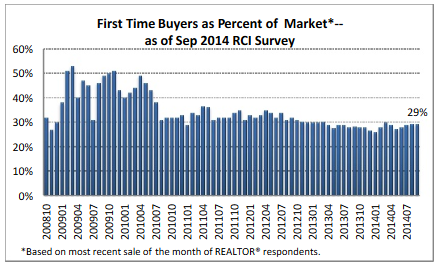

The NAR released a report which showed the first time buyer at 33% of the market during 2014. This is lowest level for this market segment since 1987, when it hit 30%. However, recent monthly data up to and including the September existing home sales report has measured first time buying as low as 27%.

It has been well-documented that the big investment buying which drove price and volume for the last 2 1/2 - 3 years is now dissipating. The first time buyer component, despite lower interest rates and favorable mortgage finance programs offered by the FHA, is not filling the demand void being left by the investment buyer segment. If first time buyers are not buying, it means that move-up buyers are restricted in their ability to sell their home in order to purchase a more expensive home. This interdependency between 1st time and move up buyers is a critical component to the level of transaction volume for the overall housing market. If this market dynamic stalls or deteriorates, I believe that the housing market could suffer a steep decline.

And its been happening in San Francisco since mid 2013. Who cares about SF real estate and first time buyers? Why is this relevant or important to me, oh Nattering One? Now, now Georgie and all you baby ducks, read below about the harbinger of death for all asset balloons and market bubbles...

Harry Dent (not Harvey from Gotham) at Seeking Alpha notes in Critical Mass For San Francisco Housing Market, re: Tyler Durden's cogent observation on 10/28/2014 at Zero Hedge in This Has Never Happened Before Without A Massive Bubble Bursting:

(Chart below) Note how this index [Case Shiller S&P San Francisco Housing Price Index Y over Y % increase] led the dot-com bubble crash and the tech wreck. It was down from early 2000 into mid- to late 2001. The Nasdaq crashed 79% from March 2000 to October 2002. This was the highest bubble in San Francisco reaching 31% before caving with the biggest stock bubble burst of our lifetime to follow.

After dropping to a low of -7%, the next rise took home prices there to a high of +24% in early 2005, just before the housing bubble peaked the following year. Since that was a real estate crash in essence, San Francisco saw one of the worst declines year-over-year, dropping a staggering -33% just from late 2007 to late 2008.

Overall real estate crashed 34% from top to bottom and that number is even greater than those from the Great Depression. Stocks crashed nearly 55% from late 2007 into early 2009.

The next round of rising home price gains in San Francisco were more limited as it was a short response to the first and most massive Fed stimulus (QE1). That advance peaked at +19% gains and was quickly countered by the sovereign debt crisis in Europe.

The index fell to -6% in late 2012 and stocks in the U.S. had their only major correction of the 2009 to 2014 bull market, down 20% into late 2011.

This latest bubble in San Francisco has been one of the largest in the U.S. since 2012 and has taken annual gains that reached a high of +26% in early 2013. Since then the index has fallen to +9%… a dramatic swing of 17 percentage points.

At this rate, all else equal, San Francisco home prices will slide into negative territory in another 5-6 months: only the fourth time they have done so in the past two decades.

As the chart demonstrates, there has never been a time when the all important leading indicator that is the San Fran housing market has posted such a steep slowdown in annual price increases without a bubble of some sort, be it the dot com, the first housing or the European sovereign debt bubble, having burst.

The reason that San Francisco is unique is that it's very bubbly from a very limited supply… it reflects both Silicon Valley and the tech bubble… and it also reflects the "mega" bubble that is China.

The Chinese dump a lot of money into the San Francisco area and when they stop it's a sign that something is wrong…

So: will this time finally be different?

The Nattering One muses... cogent observations from Kransler, Durden and Dent, who knew about the Frisco pops first syndrome? Maybe Pennywise did. A confluence of global economic declines in Germany (Euroland), China and a spending pullback from the more affluent who can still afford to spend (particulary in the U.S.) could make this big fat asset balloon go POP! And afterwards? As Pennywise the Clown said...

The NAR released a report which showed the first time buyer at 33% of the market during 2014. This is lowest level for this market segment since 1987, when it hit 30%. However, recent monthly data up to and including the September existing home sales report has measured first time buying as low as 27%.

It has been well-documented that the big investment buying which drove price and volume for the last 2 1/2 - 3 years is now dissipating. The first time buyer component, despite lower interest rates and favorable mortgage finance programs offered by the FHA, is not filling the demand void being left by the investment buyer segment. If first time buyers are not buying, it means that move-up buyers are restricted in their ability to sell their home in order to purchase a more expensive home. This interdependency between 1st time and move up buyers is a critical component to the level of transaction volume for the overall housing market. If this market dynamic stalls or deteriorates, I believe that the housing market could suffer a steep decline.

And its been happening in San Francisco since mid 2013. Who cares about SF real estate and first time buyers? Why is this relevant or important to me, oh Nattering One? Now, now Georgie and all you baby ducks, read below about the harbinger of death for all asset balloons and market bubbles...

Harry Dent (not Harvey from Gotham) at Seeking Alpha notes in Critical Mass For San Francisco Housing Market, re: Tyler Durden's cogent observation on 10/28/2014 at Zero Hedge in This Has Never Happened Before Without A Massive Bubble Bursting:

(Chart below) Note how this index [Case Shiller S&P San Francisco Housing Price Index Y over Y % increase] led the dot-com bubble crash and the tech wreck. It was down from early 2000 into mid- to late 2001. The Nasdaq crashed 79% from March 2000 to October 2002. This was the highest bubble in San Francisco reaching 31% before caving with the biggest stock bubble burst of our lifetime to follow.

After dropping to a low of -7%, the next rise took home prices there to a high of +24% in early 2005, just before the housing bubble peaked the following year. Since that was a real estate crash in essence, San Francisco saw one of the worst declines year-over-year, dropping a staggering -33% just from late 2007 to late 2008.

Overall real estate crashed 34% from top to bottom and that number is even greater than those from the Great Depression. Stocks crashed nearly 55% from late 2007 into early 2009.

The next round of rising home price gains in San Francisco were more limited as it was a short response to the first and most massive Fed stimulus (QE1). That advance peaked at +19% gains and was quickly countered by the sovereign debt crisis in Europe.

The index fell to -6% in late 2012 and stocks in the U.S. had their only major correction of the 2009 to 2014 bull market, down 20% into late 2011.

This latest bubble in San Francisco has been one of the largest in the U.S. since 2012 and has taken annual gains that reached a high of +26% in early 2013. Since then the index has fallen to +9%… a dramatic swing of 17 percentage points.

At this rate, all else equal, San Francisco home prices will slide into negative territory in another 5-6 months: only the fourth time they have done so in the past two decades.

As the chart demonstrates, there has never been a time when the all important leading indicator that is the San Fran housing market has posted such a steep slowdown in annual price increases without a bubble of some sort, be it the dot com, the first housing or the European sovereign debt bubble, having burst.

The reason that San Francisco is unique is that it's very bubbly from a very limited supply… it reflects both Silicon Valley and the tech bubble… and it also reflects the "mega" bubble that is China.

The Chinese dump a lot of money into the San Francisco area and when they stop it's a sign that something is wrong…

So: will this time finally be different?

The Nattering One muses... cogent observations from Kransler, Durden and Dent, who knew about the Frisco pops first syndrome? Maybe Pennywise did. A confluence of global economic declines in Germany (Euroland), China and a spending pullback from the more affluent who can still afford to spend (particulary in the U.S.) could make this big fat asset balloon go POP! And afterwards? As Pennywise the Clown said...

Comments